2017 Obamacare Open Enrollment

Hard to believe that we are on the fourth year for Obamacare in North Carolina. Time sure does fly.

If you have been putting off enrolling in Obamacare or need to change your coverage this needs to be completed during November 1 2016 – January 31 2017. The chart below shows when a new plan will go into effect based on the date the application is submitted:

| Application Date | Policy Effective Date |

|---|---|

| 11/1/16 – 12/15/16 | 1/1/17 |

| 12/16/16 – 1/15/17 | 2/1/17 |

| 1/16/17 – 1/31/17 | 3/1/17 |

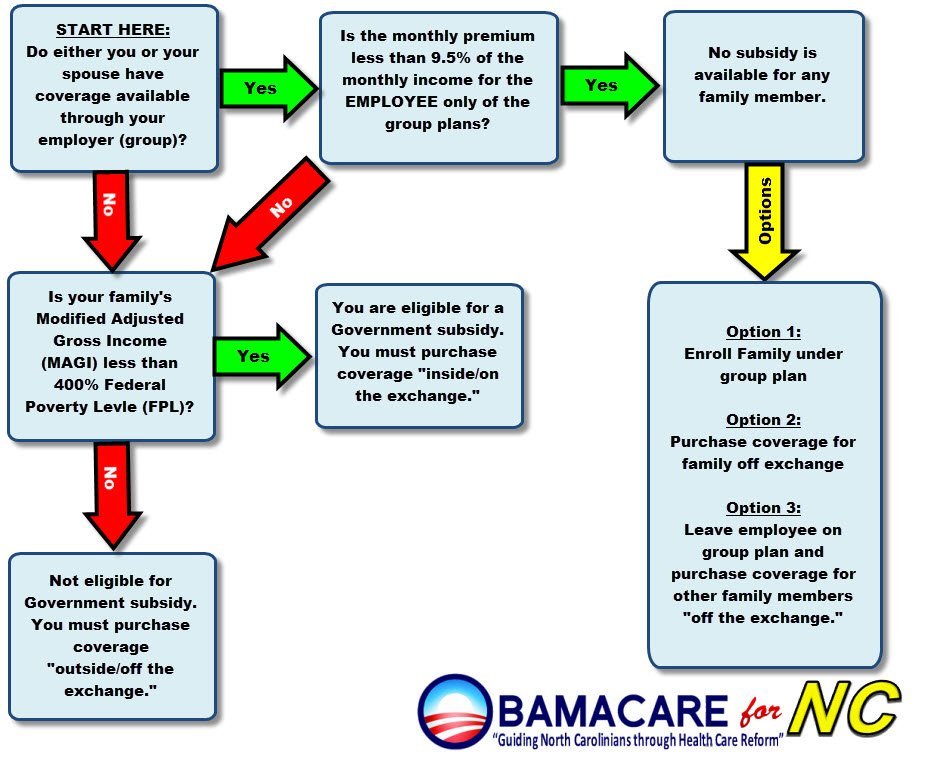

To qualify for subsidies through the health insurance marketplace for Obamacare coverage in 2017 you must meet the following requirements:

- Cannot have access to employer coverage. If coverage is offered through your employer or your spouses employer you are most likely not eligible for subsidies through the marketplace.

- Must have Modified Annual Gross Income (MAGI) between 100 – 400% Federal Poverty Level. See this page for the chart to see if you fall in the income range

Over the first 3 years of Obamacare in North Carolina we have assisted over a thousand individual obtain coverage properly and effieciently. Here is how we can help you:

- Explain the subsidy process and help ensure you get the maximum subsidy amount based on your information.

- Help you retain your subsidy throughout the year by making sure that proper documentation is submitted when required.

- We are licensed insurance professionals that are contracted with the carrier (s) that participate in the marketplace. This allows us to explain to you the benefits of the policy and why one may be better than the other. You don’t get this doing it yourself or calling healthcare.gov.

- Help you enroll in the plan that YOU choose making sure that you understand and receive maximum benefits offered.

- We do all this remotely so you never have to leave your home nor doyou don’t have to get dressed up to meet someone. Everything is handled over the internet and phone! Very simple and convenient process.

- Absolutely NO COST to you. We are compensated by the insurance companies and by using us the plans DO NOT cost any more.

So if you are reading this and YOU ARE NEW TO THE MARKETPLACE we would like to help you. Simply fill out the form to the right or click the button below. Either Rustty Williams or Kent Kingsley will contact you to review your situtation. The whole process should take less than 30 minutes and often times less.